Follow Ricardo plc for regular updates

Follow Ricardo plc for regular updatesfor trucks will be needed across Europe by 2030

Electric Vehicle Transition - A Fleet Operator's Dilemma

19 Jun 2024

SHARE

The race to decarbonise road transport is on and the role of fleet operators and owners has become increasingly complex.

The pace of change across the technological, commercial and regulatory landscapes is unprecedented, with fleet operators asked to navigate rapidly changing pressures in a highly competitive and cost-focussed market. This is no simple task.

This article focuses on battery electric vehicles and commercial medium- and heavy-duty fleets, although most of the challenges also apply to light duty fleets and other zero emission vehicle technologies. Many OEMs also expect hydrogen to play a role, particularly in the longer-haul truck and coach segments (which I will address in a future article).

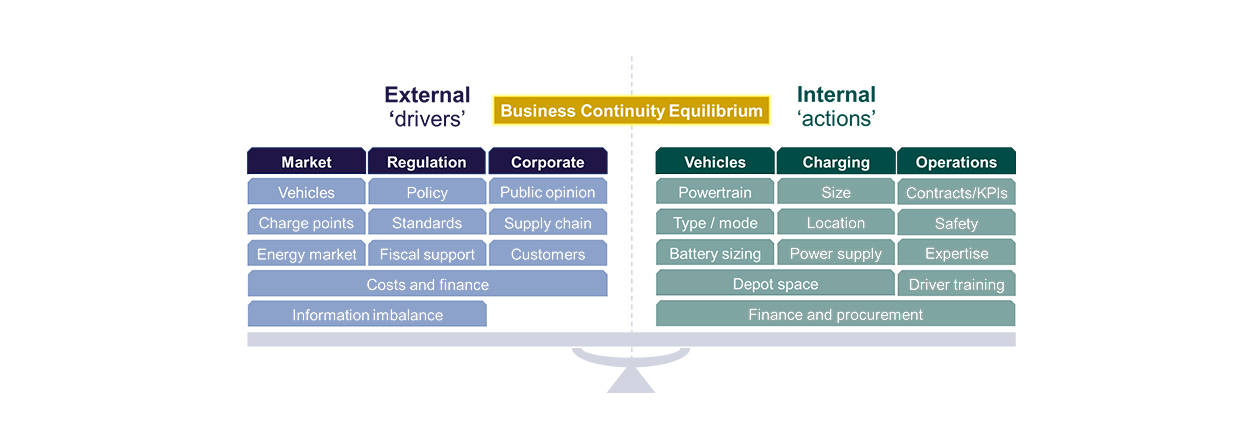

Given the critical role of transport fleets in the economy, the overarching goal is maintaining or improving business operations whilst embarking on the decarbonisation journey. What this calls for is a careful balancing act between external drivers, such as market and regulatory developments, and internal business factors, such as technology investment decisions and financing strategies.

The figure above summarises the weights on each side of the scale. For example, vehicle emission standards and petrol and diesel new sales phase-out dates are key regulatory factors influencing procurement decisions by fleet owners. Meanwhile, a lack of awareness and misinformation are both contributing to delays in the transition to cleaner fleets.

In response to the external drivers, important decisions have to be made around the powertrain composition of a fleet, the installation of charging infrastructure, and what support must be given to drivers and technicians to ensure safe and efficient operations.

Below, we take a closer look at some of the components on either side of that equilibrium and reflect on the imperative to make progress in the green fleet transition.

“The time to start transitioning is now, otherwise you risk being at the back of the queue for vehicles and may lose competitive advantage. It’s not going to be easy, cheap or quick, but collaboration between fleet operators, customers, energy suppliers and trusted partners will help to accelerate the transition.”

Tom Nokes

Senior Consultant

Vehicle technology choice and operations

There are a range of considerations that feed into the optional choice of zero emission vehicles: duty cycle, contracts, operating terrain, and depot facilities, to name just a few. To further complicate things, the order that decisions are made can also influence the success of vehicle adoption. We see real-world examples where decisions were made on the vehicle without considering depot space and power availability, resulting in costly and long delays.

Considering that the range of electric trucks is smaller than conventionally powered trucks, there will be implications on driving hours, rest periods and payload. Given the different operational characteristics of electric vehicles, it’s important to focus on meeting the objectives of the fleet rather than trying to mimic how it is operating today.

We supported a multinational consumer goods company to assess alternatives for their diesel-powered refrigerated trailers.

The refrigerated trailers carry a significant environmental impact and so switching trailers onto alternative fuels can notably improve a fleet’s emissions.

While power take off (PTO) (taking energy from the tractor battery) works well for rigid trucks, articulated trucks do not yet have standardised high-power connections between the tractor and trailer, and tractor range is reduced. Alternatively, a transport refrigeration unit (TRO) gives the trailer “autonomy”, but it adds cost, reduces the payload and means the trailers need to be charged, which complicates logistics.

Beyond refrigerated transport, Ricardo has experience supporting other specialist vehicle fleets, including waste, emergency services and military.

Charging and route management

The question of battery sizing is vital when specifying battery electric heavy duty vehicles (HDVs), and it can be tempting to select the biggest battery possible.

However, this impacts cost, payload, efficiency and end-of-shift charge time, and even the biggest batteries available will not give you the range of a diesel truck.

This means that truck routes and charging strategies should be carefully planned. In general, trucks with shorter duty cycles can rely on overnight charging at the depot but long-haul operations will require top-up charging en route. This could be at a customer or supplier depot, or utilising public infrastructure.

Across this private and public charging landscape, there are two important considerations:

- Many depots are leased and may not have adequate power or space for EV charging, so decisions about where to electrify might place more emphasis on the suitability of depots rather than the easiest routes. There’s an important opportunity here for collaboration between fleet operators, customers, depot owners and suppliers to support charging en route.

- Requirements on rest times for truck drivers could be aligned with public charging to avoid disruption on longer journeys. However, public charging infrastructure for trucks in Europe is simply not there yet and deploying the 50,000 high powered chargers needed by 2030 will require a significant acceleration in infrastructure investment (according to the European Automobile Manufacturers' Association - ACEA).

Using Ricardo’ charger route model (ChaRM), we worked with a transport authority to identify optimal locations for charge points across their bus routes, minimising the total cost of the network.

In this example, it generally became more cost effective to run opportunity charging for buses with duty cycles over 275km, due to the battery sizing trade off. Although once initial charge point installations were considered, it created cost optimal opportunities for shorter duty cycle buses with overlapping routes.

The model can also assign optimal zero-emission technology options for routes and works with a range of fleet types (buses, RCVs, delivery) and different geographies.

50,000

High-powered charging points

Depot operations and safety

Depots and operations are set up for conventional transport fuels so the transition to electric and hydrogen fleets changes all this. Everyone will require basic training, and maintenance teams will require retraining.

Even with fuel cell vehicles, high voltage training is required.

Working areas may also need to be modified along with guidance on safe working practices. For example, untrained staff should be kept away from vehicles during maintenance.

An international mining company was beginning to switch its large mining trucks to hydrogen fuel cell, but discovered there was no off-the-shelf safety training available.

Ricardo delivered bespoke, in-person JOIFF* accredited training on awareness, safety and incident response in relation to hydrogen, fuel cells and lithium-ion batteries to over 30 of the customer’s operations professionals and local firefighters

*JOIFF is the International Organisation for Industrial Emergency Services Management

Financing and procurement

Procurement is more complex than just buying a vehicle and a charger – it encompasses a range of other financial considerations across operations, infrastructure and energy.

For example, changing vehicle maintenance contracts might encourage leasing over ownership, and there are emerging business cases for on-site renewable generation.

The major consideration for transport fleets is total cost of ownership (TCO), and the headline is that battery electric trucks are not yet economically attractive, but are expected to be competitive from mid-2020s depending on their use. Trucks used for regional distribution achieve TCO parity ahead of longer-haul trucks due to their smaller battery requirement and more favourable duty cycle.

In 2023 and 2024, the high levels of inflation and interest rates made fleet procurement a challenge. Which makes finding subsidies doubly important - they won't be around forever so there is a first mover advantage. Furthermore, subsidies and grants often don't apply to leased vehicles, and certainly not to grey fleet (employee owned vehicles), so it may be necessary to re-evaluate the ownership model.

The emergence of as-a-service solutions for vehicles and charging can ease the burden on the transport manager and the company balance sheet, but they need careful evaluation before signing a long-term contract. Making use of a trusted partner to evaluate the complex options can ease the burden on the fleet manager and ensure the right decision is made for the company.

Ricardo recently delivered a study to European Clean Trucking Alliance (ECTA) on financing mechanisms for zero emission trucks and their infrastructure.

Our report highlighted the challenges for smaller companies who dominate the fleet market. Even when TCO is positive, these fleets often cannot afford the upfront investment on vehicles and infrastructure. Therefore, they will look to the market for loans or leases, but the market typically offers worse terms for alternatively fuelled vehicles. Our recommendations can be read here.

The case for electrifying

Despite the challenges, it’s worth remembering the strength of the case for electrifying fleets.

It can position organisations favourably with customers and, as well as reducing emissions, there are benefits around driver retention, recruitment, and diversity. The vehicle business case is improving and there are regulatory pressures that are already signalling the end of fossil fuelled powered vehicles.

Some regions have favourable conditions that may enable faster fleet electrification across all vehicle types. Europe, for example, is a relatively densely populated area with a reliable and greening grid, offers affordable finance, and has strong legislation. Regions with less favourable conditions are likely to see more hesitancy around the adoption of electric trucks, especially for longer-haul transport.

In summary

The scales will never be perfectly balanced for a fleet operator, not least because business, regulation and technology are rarely perfectly aligned. However, the time to start the transition is now, otherwise you risk being at the back of the queue for vehicles and power and may lose a competitive advantage. It’s not going to be easy, cheap or quick but collaboration between fleet operators, customers, energy suppliers and trusted partners will help to to accelerate the transition.